Financial Sector Development Policies

The objective of Financial Sector Development Policies is to promote inclusive development of the financial sector. On this page, you will find two Financial System Development Policies issued by the Reserve Bank, including:

- Financial Sector Development Policy Statement No. 1 on Minimum Requirements for the Provision of Disaggregated Data; and

- Financial Sector Development Policy Statement No. 2 FinTech Regulatory Sandbox Guideline.

- Financial Sector Development Policy Statement No. 3 Policy for the Protection and Fair Treatment of Financial Consumers

Financial Sector Development Policy Statement No. 1

Minimum Requirements for the Provision of Disaggregated Data

This Policy sets out the Reserve Bank of Fiji’s (RBF) minimum requirements for the provision of disaggregated data on financial inclusion by Financial Service Providers (FSPs) licensed and supervised by RBF.

The purpose of the Policy is to ensure that FSPs standardise, collate and report disaggregated financial inclusion data by “gender”, “location” and “age” to the RBF. FSPs are required to report on bank account ownership (deposits and loans), mobile money wallet ownership, payment services, payment instruments, MSME financing, life and general insurance, capital market investments, superannuation, and personal remittances. The Policy strengthens data availability and quality, assists in policy formulation, monitoring and evaluation of financial inclusion in Fiji’s financial system.

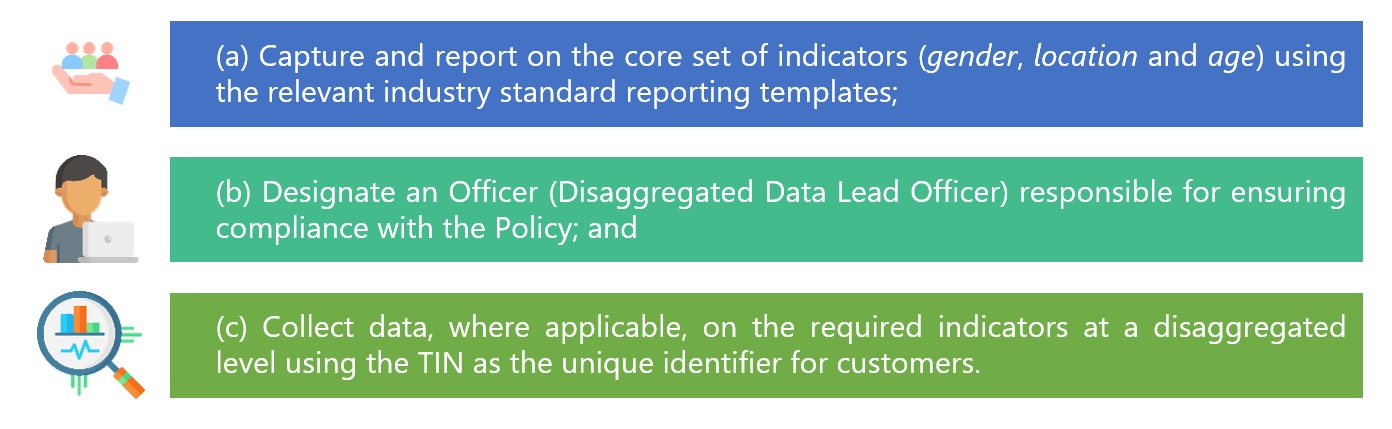

Under the Policy, each FSP is required to:

This Policy came into effect on 01 June 2019. FSPs are currently required to provide annual data as at 31 December of each year to the RBF by 31 March of the following year (within 3 months after the end of the calendar year).

Download here:

Financial Sector Development Policy Statement No. 2

FinTech Regulatory Sandbox Guideline

This Policy outlines the RBF’s minimum requirements or guidelines for admitting a proposed product solution for testing in RBF’s FinTech Regulatory Sandbox.

The Guideline sets out the terms of the Sandbox and is targeted for firms that have developed solutions and technologies in an innovative way to improve the delivery of financial services that fall within the ambit of the RBF. These include financial service providers that are licensed and supervised by the RBF, FinTech firms and where applicable, individuals and other firms not primarily in the business of providing financial services with technology-based solutions.

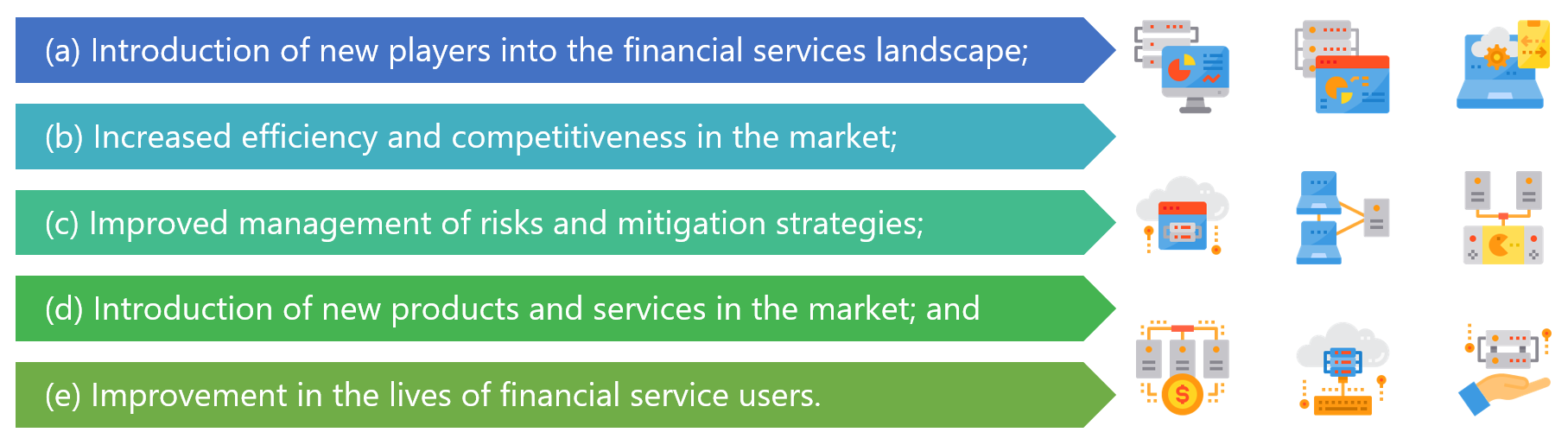

The purpose of the Policy is to provide a framework that will allow FinTech and other solutions to be tested in a live environment within approved and specified parameters and timeframes. The framework is therefore an approach to fostering responsible innovation that allows for:

Interested applicants are required to familiarise themselves with the objectives and principles of the sandbox. The Sandbox cannot be used as a means to circumvent existing regulatory and legislative requirements.

Early consultation with the RBF prior to submission is recommended. This Guideline is effective from 31 December 2019.

Download here:

Financial Sector Development Policy Statement No. 2 FinTech Regulatory Sandbox Guideline

Entities Admitted to the Experimentation Stage of the FinTech Regulatory Sandbox

| Entity | Solution | Period |

| Pacific Insurance and Climate Adaptation Programme | Group Parametric Micro-insurance Product offered to selected Agri-based co-operatives that provides predetermined pay-outs based on weather perils that meet predefined triggers. The Product is supported by a weather modelling and calculating agency and a digital on-boarding platform. Further information of the programme is linked here. | December 2021 to April 2023

Status: Complete |

| Vodafone Fiji Pte Limited | A companion card linked to e-money on M-PAiSA accounts and co-badged to MasterCard, enabling its users to transact on both local and overseas EFTPOS terminals, ATMs and online payment gateways on the MasterCard network. Further information of the product can be found here. | August 2022 – March 2023

Status: Complete |

| Dynamic Payment Limited | Single-use, non-reloadable prepaid gift cards sold in fixed denominations in local currency over-the-counter at selected participating merchants and used for payments at merchants whose EFTPOS terminals accept China Union Pay. The cards cannot be redeemed for cash at merchants or ATMs. | September 2022 – May 2023

Status: Complete |

| SOLE Limited | A multi-feature financial management platform developed around an electronic wallet at its core which provides the ability to create sub-accounts or ‘buckets’ for user-defined purposes including payment obligations and financial goals. The electronic wallet’s functions are limited to domestic transactions only. | October 2022 – April 2023

Status: Complete |

Financial Sector Development Policy Statement No. 3

Policy for the Protection and Fair Treatment of Financial Consumers

This Policy outlines the minimum requirements to ensure fair and responsible treatment of financial consumers in their interactions with financial services providers.

The objective of the Policy is to:

a) Provide the minimum requirements for FSPs on the standards of fair practice in the delivery of their financial products and services, transparency and disclosure of the key product information which enable consumers to make informed financial decisions; and

b) Ensure that the board and senior management of the FSPs promote fair treatment of consumers consistent with Prudential Supervision Policy Statement No. 3.

This Policy comes into effect on 01 April 2024 with full compliance by FSPs required within 12 months from the effective date.

Download here:

Policy:

FSDPS 3 Policy on Protection and Fair Treatment of Financial Consumers

All Guidelines (Compressed Zip Folder):

Guidelines Issued Under FSDPS 3

Links to each guideline:

Guideline 1 on Fair and Equitable Treatment of Consumers

Guideline 2 on Transparency and Disclosure

Guideline 3 on Protection of Consumer Assets Against Fraud Misuse and Scams

Guideline 4 on Protection of Data and Privacy

Guideline 5 on Complaints Handling and Redress

Guideline 6 on Financial Literacy and Awareness